Tech Stock Sell-Off: Are AI Bubble Fears Signaling a Market Correction?

Tech Giants Rocked by AI Bubble Fears: Global Market Faces Uncertainty Recent days have witnessed a dramatic downturn in global stock markets, driven largely by mounting concerns around an “AI bubble” that threatens the stability of the technology sector and the wider financial landscape. With tech valuations skyrocketing in recent years, and key investors betting against some of the biggest companies in the industry, market watchers are questioning whether current price levels are sustainable. The Trigger: Fears and Short Bets Shake Major Indexes Early November saw renewed volatility across the Nasdaq, S&P 500, and key Asian indices such as Japan’s Nikkei 225 and South Korea’s Kospi. Tech titans like Apple, Amazon, Microsoft, and Alphabet all posted substantial losses, while the semiconductor sector—integral to AI infrastructure—witnessed a staggering $500 billion drop in market value. These shocks were amplified by notable short positions from prominent investors like Michael Burry, who gained international fame for predicting the 2008 financial crisis. Burry’s decision to take a massive short position against leading AI stocks Palantir and Nvidia injected fresh anxiety into the market. Statements from market insiders, including hedge fund chiefs and Wall Street executives, have further inflamed speculation that an overheated AI sector could lead to a broader correction. Valuations Detach from Fundamentals One of the most significant warning signs is the apparent disconnect between sky-high valuations of AI and tech firms and their actual economic resilience. Palantir, for example, was recently valued at over 300 times its projected 2025 earnings, and the S&P 500’s forward price-to-earnings ratio now mirrors levels seen before the dot-com crash. While the promise of AI-driven innovation continues to attract huge inflows of capital, a growing body of analysts caution that much of this investment is based on speculative momentum, rather than demonstrated profitability. The AI Investment Frenzy and Mixed Results The world’s top technology companies have collectively invested over $400 billion in AI infrastructure this year alone. However, a study by MIT found only 5% of more than 300 corporate AI projects have delivered measurable benefits, with most stalling in pilot phases due to integration and scalability issues. While cloud computing giants like Amazon Web Services, Microsoft Azure, and Google Cloud are seeing revenue growth thanks to AI processing demand, their profit margins are under increasing strain due to surging infrastructure costs. This mismatch between investment and profit has raised echoes of previous speculative bubbles. Interconnected “circular” deals—where companies invest in each other’s AI projects—are drawing comparisons to the late 1990s, when similar patterns contributed to the dot-com bust. Global Implications: Ripple Effects Beyond Big Tech The risk-off sentiment has not only hammered tech stocks in the U.S. but also sent shockwaves through Asian and European markets. The Nikkei 225 posted its biggest drop in seven months, reflecting the global nature of current fears. Even digital assets like Bitcoin briefly plunged as investors sought safer havens amid uncertainty. Meanwhile, “Magnificent 7” stocks—including Apple, Amazon, Microsoft, Alphabet, Meta, Tesla, and Nvidia—have accounted for the overwhelming majority of S&P 500 gains in recent months, deepening worries about a narrow and vulnerable rally. CEO and Regulator Warnings Raise the Alarm Financial leaders at Goldman Sachs and Morgan Stanley have sounded the alarm at investment summits, warning of potential 10–20% corrections in tech-heavy indices if sentiment doesn’t turn soon. The sharpness of recent sell-offs underscores concerns that any slowdown or negative news could quickly cascade, erasing billions more in value and challenging the optimism surrounding artificial intelligence’s market impact. Silicon Valley’s Financial “Arms Race” Vast sums are being spent on new data centers and next-generation AI chips, leaving only the largest companies able to compete at the highest level. This “financial arms race” is creating tough barriers for smaller firms, setting the stage for possible market consolidation and shakeouts if the bubble bursts. Reports reveal that up to 95% of generative AI initiatives fail to achieve notable revenue growth, spotlighting the risks tied to speculative capital infusions and raising questions about the most likely survivors in a potential downturn. Lessons from History: Is a Market Correction Imminent? The present environment bears striking similarities to past speculative mania, notably the dot-com bubble, where a rush of investor optimism was eventually met with harsh financial reality. As tech stocks correct and warnings multiply, experts stress the importance of disciplined investment strategies and a renewed focus on genuine, long-term profitability in the AI sector. Conclusion: Navigating an Uncertain Future While artificial intelligence continues to inspire massive investments and transform business strategies, current market turbulence is a stark reminder of the dangers of runaway valuations. As scrutiny intensifies and short interest rises, investors are urged to distinguish real innovation from hype and focus on fundamentals to weather the possible storm ahead.

Decoding DeFi: Can Decentralized Finance Outshine Traditional Banking?

The financial world is in the middle of a tectonic shift. For centuries, centralized institutions, banks, governments, and credit agencies have acted as the backbone of global finance. But the rise of Decentralized Finance (DeFi) has challenged this traditional system, offering an alternative built on transparency, autonomy, and blockchain technology. Supporters argue that DeFi could democratize access to financial services and reduce dependence on intermediaries. Skeptics warn of volatility, security risks, and lack of regulation. So, can DeFi really outshine traditional banking, or is it destined to remain a niche alternative? Let’s decode DeFi, understand its opportunities and challenges, and weigh its potential to reshape the global financial order. What is Decentralized Finance? At its core, Decentralized Finance refers to financial services built on blockchain networks, most commonly Ethereum, where transactions occur without traditional intermediaries like banks or brokers. Instead, DeFi uses smart contracts, self-executing programs coded on blockchains, that automatically enforce rules and agreements. Decentralized Finance encompasses a wide array of services, including: In short, DeFi aims to replicate, and eventually surpass, traditional banking functions on a decentralized, open infrastructure. The appeal: Why DeFi is gaining traction DeFi’s rise is not accidental. Several core features explain why millions of users and billions of dollars in capital have flocked to this space. 1. Accessibility and financial inclusion Traditional banking often excludes people, whether due to geography, lack of documentation, or credit scores. DeFi, being internet-based, is globally accessible to anyone with a smartphone and a crypto wallet. For the unbanked or underbanked populations (estimated at 1.7 billion worldwide), DeFi offers an entry into financial services without relying on centralized gatekeepers. 2. Transparency and trust through code In traditional finance, customers trust institutions to safeguard assets, maintain ledgers, and follow regulations. In DeFi, transactions and smart contracts are visible on public blockchains. This radical transparency builds trust not through institutions, but through code and consensus mechanisms. 3. Control and autonomy Users in DeFi have full custody of their funds. Unlike banks, which can freeze accounts or impose transaction limits, DeFi empowers individuals with sovereignty over assets. This appeals strongly to those skeptical of centralized power. 4. Efficiency and lower costs DeFi eliminates intermediaries. A loan or transfer that requires banks, clearinghouses, and multiple fees in traditional systems can happen directly, often at lower cost and higher speed. 5. Innovation and composability DeFi platforms are “money Legos”, applications can be combined, layered, and built upon one another. For example, a user can deposit stablecoins into Compound, receive interest-bearing tokens, then stake those tokens in another protocol for additional yield. This flexibility fosters a culture of relentless experimentation. Traditional banking’s stronghold While DeFi is disruptive, traditional banking still holds enormous advantages. It remains the dominant system for several reasons: 1. Stability and trust built over centuries Banks, despite crises and scandals, are deeply embedded in societies. People trust them with salaries, mortgages, retirement accounts, and day-to-day payments. DeFi, by contrast, is relatively new and still viewed by many as experimental. 2. Fiat integration and government backing National currencies are issued, guaranteed, and stabilized by governments and central banks. DeFi stablecoins, while useful, ultimately rely on traditional financial systems to maintain their pegs. 3. Regulation and consumer protection Banks are heavily regulated to protect depositors, prevent fraud, and ensure systemic stability. Customers enjoy protections like deposit insurance (FDIC in the U.S., for example), dispute resolution, and legal recourse. DeFi users have little recourse if they lose funds due to hacks or contract bugs. 4. Scale and infrastructure Traditional finance manages trillions of dollars across global markets. While DeFi has grown quickly, peaking at over $200 billion in Total Value Locked (TVL) in 2021, it is still a fraction of global banking assets, which exceed $400 trillion. 5. Integration with the real economy Banks provide credit that powers businesses, infrastructure, and governments. DeFi’s reach into real-world economic activity is still limited, with most activity confined to speculative trading and crypto-native assets. Can DeFi outshine banking? The case for yes 1. Disintermediation is powerful By removing layers of middlemen, DeFi can make financial systems faster, cheaper, and more efficient. Just as e-commerce disrupted retail, DeFi could disrupt banking by directly connecting lenders with borrowers, savers with investors. 2. Global inclusivity DeFi has the potential to leapfrog traditional barriers, especially in regions with weak banking infrastructure. Just as mobile money revolutionized payments in parts of Africa, DeFi could unlock lending, savings, and investment services globally. 3. Programmable money unlocks new possibilities Traditional contracts are costly and slow to enforce. Smart contracts automate agreements, reducing risk and administrative burden. From microloans to automated insurance payouts, the scope is vast. 4. Resilience and censorship resistance Because DeFi is decentralized, it’s harder for governments or institutions to censor or control. For individuals in authoritarian regimes or unstable economies, this can be life-changing. 5. Pace of innovation Traditional finance moves slowly under regulatory and bureaucratic constraints. DeFi’s open-source, composable nature means new financial products can launch in days. Innovation cycles are rapid, fueling continuous improvement. Or will banking still win? The case for no 1. Volatility and instability: The crypto ecosystem is notoriously volatile. The collapse of TerraUSD in 2022 wiped out billions, shaking confidence in DeFi’s stability. Banks, despite flaws, are backed by central banks that can stabilize crises. 2. Security risks and hacks: Smart contracts are vulnerable to bugs, exploits, and hacks. Billions of dollars have been stolen from DeFi protocols in recent years. Without insurance or consumer protections, users bear the losses. 3. Complexity and user experience: Managing private keys, navigating wallets, and understanding protocols can be daunting for the average user. Banks, with user-friendly interfaces and customer support, remain far more accessible. 4. Regulatory headwinds: Governments are unlikely to relinquish control over monetary systems. Many regulators are already imposing stricter rules on DeFi, targeting stablecoins, exchanges, and lending platforms. Heavy regulation could stifle growth or force DeFi into hybrid models reliant on centralized compliance. 5. Lack of real-world integration: Most DeFi activity remains within the crypto

Adobe MAX 2025: Firefly Foundry Redefines Enterprise AI Creativity

Adobe MAX 2025 Ushers in a New Era for Enterprise AI Creativity Adobe’s annual MAX conference in Los Angeles captured global attention in late October 2025, unveiling a bold new platform strategy designed to transform creative business workflows at scale. Center-stage was the introduction of Firefly Foundry, a fully managed AI service tailored for large enterprises seeking proprietary, on-brand content generation, coupled with strategic partner integrations, enhanced pricing models, and the expansion of Adobe’s Content Authenticity Initiative. Firefly Foundry: Enterprise AI Model Creation Firefly Foundry is Adobe’s answer to the growing demand for customized, secure AI solutions in the enterprise market. Unlike previous approaches, Firefly Foundry allows organizations to collaborate directly with Adobe experts, including PhDs and advanced AI engineers, to build multi-year, deeply tuned generative AI models based entirely on proprietary brand assets and guidelines. The Foundry empowers brands to scale content production, streamline marketing workflows, and extend creative reach, all while maintaining rigorous controls over brand voice and data security. Seamless Platform Integration & Expanding Partner Ecosystem Adobe’s vision for Firefly Foundry extends across its powerful creative ecosystem—including GenStudio, Creative Cloud, and Express—enabling businesses to deploy AI assets efficiently and safely. The company also announced integrations with leading AI providers like Google, OpenAI, ElevenLabs, and Runway, further enriching the Firefly platform’s capabilities. Adobe’s “commercially safe AI vendor” positioning is reinforced by exclusive use of licensed and public domain data for model training, critical as content standards and regulations tighten globally. Consumption-Based Pricing Redefines Enterprise Flexibility A major shift for enterprise customers is Adobe’s adoption of a consumption-based pricing structure. Teams now purchase “generative credits” that act as currency across AI features in Creative Cloud, with each subscription offering a baseline amount: Content Authenticity Advances and Compliance Initiatives Recognizing rising regulatory and ethical standards around AI-generated content, Adobe expanded its Content Authenticity Initiative at Adobe MAX 2025. Over 50 products now participate in the conformance program, focused on content provenance, creator attribution, and compliance with regulations like the EU AI Act and California AI transparency laws. Strategic Impact and Industry Leadership Adobe’s enterprise-focused announcements at Adobe MAX 2025 reflect a decisive pivot toward comprehensive, scalable creative solutions. With Firefly Foundry, robust partner integrations, and a flexible pricing model, Adobe aims to help organizations overcome production bottlenecks and fuel innovation at every stage of content creation. As AI adoption accelerates, Adobe is setting itself apart through responsible innovation, strategic partnerships, and a platform designed to serve the entire spectrum of creative needs in the enterprise market. For more insights, subscribe The Business Tycoon

From Wallets to Wearables: The Next Frontier in Digital Payments

The world of money is changing faster than ever. Not long ago, cash was king, and the idea of paying for a coffee with your phone seemed futuristic. Then came digital wallets, apps like PayPal, Apple Pay, Google Pay, and Venmo, that redefined how we transact. Today, we are on the cusp of yet another shift: wearable technology is emerging as the next frontier in digital payments. From smartwatches that let you tap to pay, to rings and fitness trackers embedded with payment capabilities, the very act of making a purchase is evolving into something more seamless, secure, and integrated into our daily lives. The question is no longer if wearables will shape the future of payments, but how far and how fast. The Journey from Physical to Digital Payments To understand why wearables are the next big leap, it’s worth tracing the path of payment evolution. Each phase solved a problem of the previous one, wearables now promise ultimate convenience, speed, and personalization. What Are Wearable Payments? Wearable payments use NFC, Bluetooth, or biometric authentication embedded into smart devices to enable secure, contactless transactions. Examples include: Instead of reaching for your phone or card, you simply tap your wearable to a terminal, and the transaction is complete. Why Wearables Are the Future of Payments 1. Seamless Convenience Wearables are always on you. No digging through pockets or bags for cash, cards, or phones, payment is literally at your fingertips. 2. Enhanced Security Biometric features like fingerprint, face ID, and heart rate recognition add layers of authentication that cards cannot match. Most wearables also use tokenization, meaning sensitive card data is never exposed. 3. Hygienic & Contactless In a post-pandemic world, touchless interactions are preferred. Wearable payments minimize physical contact, aligning with consumer safety habits. 4. Integration with Lifestyle Wearables are not just about payments, they track health, fitness, and daily habits. Adding payments creates a centralized ecosystem of personal data and convenience. 5. Global Acceptance With 85% of point-of-sale systems worldwide now NFC-enabled (per Mastercard), wearables can be used almost anywhere cards are accepted. The Market Potential: Numbers Speak Volumes These figures highlight not just a trend but a paradigm shift in consumer behavior. Use Cases Across Industries Retail Shoppers breeze through checkout lines by tapping their smartwatches or rings, enhancing customer experience and reducing queues. Healthcare Patients in hospitals can make payments for cafeteria meals or prescriptions using fitness trackers they already wear for health monitoring. Travel & Hospitality Airlines are experimenting with wearables that double as boarding passes and payment methods for in-flight purchases. Hotels are enabling smart wristbands that act as room keys, IDs, and wallets. Events & Entertainment At concerts and sports stadiums, smart wristbands eliminate the need for wallets or phones, speeding up concession sales. Fitness & Lifestyle Runners or cyclists no longer need to carry wallets, fitness bands with payment capabilities enable purchases mid-workout. Challenges Holding Back Wearable Payments Despite the promise, challenges exist: The Role of Tech Giants in Driving Adoption This ecosystem is growing more collaborative, suggesting a tipping point for mass adoption is near. Beyond Payments: The Superpowers of Wearables Wearables are not just about transactions, they’re becoming multifunctional lifestyle companions. The Road Ahead: What the Future Holds Conclusion: Tapping Into the Future The journey from wallets to wearables is more than a technological shift; it’s a cultural one. Wearables are not just making payments easier; they’re redefining how we interact with money in everyday life. For consumers, this means unparalleled convenience. For businesses, it means new revenue streams and faster transactions. For the world, it signals the dawn of a cashless, cardless, and frictionless economy. As adoption grows and technology advances, wearable payments won’t just be a novelty; they’ll be the new normal. The next time you buy a coffee, don’t be surprised if all it takes is a flick of your wrist. For more insights, subscribe The Business Tycoon

The AI Gold Rush: Who Will Own the Future of Artificial Intelligence?

Artificial Intelligence is not just another technology trend: in many ways, it feels like a land grab. Everyone, from tiny startups to multinational giants, from governments to universities, is racing to stake a claim in who owns the future of AI. But “ownership” in Artificial Intelligence is multi-dimensional: owning the models, owning the data, owning the infrastructure, owning the regulations, owning the ethical frameworks. This article digs into how that gold rush is unfolding, who the major claimants are, what they want, the risks, and ultimately, who may end up owning “AI.” What does “owning Artificial Intelligence” mean? Before naming names, we need to define what it might mean to own AI. Several overlapping domains of ownership are: Each layer is a lever: if you own the infrastructure, you get cost advantages; if you own the data, you can train better models; if you own the regulation, you shape what is possible. The gold rush is really about capturing control in as many of these layers as possible. Who are the major players staking their claim? Here are the key contenders across different layers, some already deeply embedded, others up-and-coming. Big Tech Giants Emerging Players, Startups & Regionals Key battlegrounds & dynamics Knowing the players, let’s see what the battlegrounds are, where the competition is fiercest, and what trade-offs are involved. 1. Compute & hardware Compute is often described as the physical foundation of AI power. Anyone can talk about clever algorithms, but training massive models requires enormous GPU/accelerator capacity, power, cooling, and data center infrastructure. Whoever controls this wins many battles. 2. Data and model access 3. Intellectual property, licensing, and regulations 4. Vertical domination vs horizontal platforms 5. Ethics, public trust, and social license Who is likely to win, and what combinations of ownership might emerge It seems unlikely that one actor will own everything. More likely, we’ll see ecosystems of layered ownership, shifting alliances, and regional variation. Here are some plausible scenarios/combinations. Scenario What Ownership Looks Like Key Players Risks / Trade-offs Horizontal superpowers A few giants control the models, infrastructure and provide AI services globally. Microsoft + OpenAI, Google, Amazon, NVIDIA. Possibly large Chinese firms in their home markets. Regulatory pushback; local data laws; public mistrust; stagnation/lack of competition; risk of monopoly. Regional specialization/fragmentation Different regions dominate different pieces: China for model/data/control in its sphere; EU with strong regulation and ethics; US with commercial/enterprise strengths; etc. Chinese firms (Baidu, Alibaba, Facebook’s counterparts), EU firms + regulators, US big tech. Risk of duplication, inefficiencies, conflict over standards, barriers to global collaboration. Vertical specialists Many domain-specific players own “AI in X” (e.g., healthcare, legal, finance, biotech), while infrastructure is shared or rented. Startups & incumbents in sectors: health AI firms, legal tech, automotive, etc. Infrastructure is from cloud providers; models possibly from OpenAI, etc. Vertical players may struggle to compete on model scale; dependency on big models/infrastructure providers; potential for lock-in. Open/hybrid ecosystem A mix of open source and proprietary; more democratic access; shared infrastructure; federated models; stronger regulation ensuring ethical practice. Open source communities (HuggingFace, etc.), startups, and non-profits, supported by regulation and maybe public funders. Slower pace (perhaps), risk of lower margins; challenge in monetization; potential IP conflicts; harder to guard against misuse. What factors will influence who wins Several trends and forces will shape which of these scenarios becomes dominant, and in which places. Risks & downsides of the gold rush The stakes are high, but there are also serious risks if ownership concentrates unfairly or carelessly. What might “ownership” look like in 2030-2035 Projecting a decade forward, here are some plausible states of the Artificial Intelligence ownership landscape. Takeaways: Who will end up owning the Artificial Intelligence future? Given everything, here are some reasoned predictions. What you should watch if you care (or want to invest) If you’re watching this space, whether as a researcher, businessperson, policy-maker, or investor, keep an eye on: Conclusion The AI gold rush is underway. It’s not simply about who builds the smartest model or the fastest chip; it’s about who controls the stack: hardware, data, software, regulation, and domain application. While giants like NVIDIA, Microsoft, Amazon, Google, and OpenAI are well positioned for much of the foundation, it’s unlikely any one player will “own it all.” Instead, we’ll see mixed ownership, shifting allegiances, regional variation, and evolving norms and laws. Ultimately, “ownership” of the future of Artificial Intelligence will be negotiated, not only in boardrooms and data centers, but in courts, legislatures, public perception, and global standards. For those who understand the multiplicity of ownership, there may still be an enormous opportunity. For those who ignore the legal, ethical, and infrastructural layers, the gold may slip through their fingers. For more insights, follow The Business Tycoon

India Win Historic First ICC Women’s World Cup 2025 Title

India’s Triumph: A New Era in Women’s Cricket India’s women’s cricket team made history by winning their maiden ICC Women’s Cricket World Cup title, overcoming South Africa by 52 runs in a landmark final at Navi Mumbai’s DY Patil Stadium. After decades of near misses and heartbreaks, India finally lifted the trophy in front of an ecstatic home crowd, marking a new chapter for women’s cricket in the country and the continent. Shafali Verma’s Explosive Batting Sets the Platform India were asked to bat first and made the most of their opportunity from the outset. Shafali Verma, the young phenom, led the charge with a blistering 87 off 78 deliveries, striking seven boundaries and two sixes. Her aggressive intent not only set the tone for the innings but also placed significant pressure on South Africa’s bowlers throughout the powerplay. Opening partner Smriti Mandhana complemented Verma with a fluent display, helping India race past the 50-run mark in under 10 overs. The duo’s partnership weathered a two-hour rain interruption and kept the home fans hopeful for a formidable total. Deepti Sharma: The All-Round Match Winner Deepti Sharma emerged as India’s star, delivering both with bat and ball when it mattered most. After contributing a crucial 58 runs in the middle order, Sharma’s exceptional bowling spell shattered South Africa’s hopes. Her figures of 5 for 39 turned the tide, making Sharma the first bowler to claim a five-wicket haul in a Women’s World Cup final. Sharma’s impact was not limited to wickets—she broke partnerships at critical junctures, most notably dismissing South African captain Laura Wolvaardt, whose century had kept her team alive in the chase. Sharma’s all-round heroics earned her widespread acclaim and cemented India’s path to victory. South Africa’s Fight Through Laura Wolvaardt South Africa’s response was led by their captain Laura Wolvaardt, who crafted a brilliant 101 off 98 balls. Despite her resolve, South Africa struggled for consistency, losing wickets at regular intervals—especially after Sharma’s breakthroughs. The rest of the lineup could not support their captain, falling short by 52 runs as they finished their innings at 246. The Influence of Coach Amol Mazumdar This historic achievement was shaped behind the scenes by head coach Amol Mazumdar, whose leadership injected new belief and discipline after a period of instability. Known for his vast domestic experience, Mazumdar redefined India’s approach with tactical acumen and motivating team talks—most notably after a close defeat to England in the group stage. The turnaround was seen in India’s spirited comeback and record chase in the semifinals, ultimately culminating in the final win. Prize Money and the Significance of Victory India’s triumph wasn’t just about sporting glory—it also came with record-breaking financial rewards. The team received a staggering USD 4.48 million (approximately Rs 39 crore), representing the highest prize purse in Women’s World Cup history and a testament to the growth of women’s cricket in India and globally. South Africa, as runners-up, also secured a significant reward, reflecting the high stakes and rising recognition in international women’s cricket. Ecstatic Celebrations and Emotional Moments The final whistle unleashed spontaneous celebrations—tears, hugs, and slogans filling the stadium. Harmanpreet Kaur lifted the trophy surrounded by smiling teammates, fans waving the national flag, and the world acknowledging India’s new position at the pinnacle of women’s cricket. Impact on Women’s Cricket in India India’s triumph in the 2025 Women’s World Cup sets in motion a new era for the sport in the country. Boosted by large viewership, media coverage, and a dramatic increase in financial support, women’s cricket has finally captured the nation’s imagination. The victory is expected to inspire a new generation of cricketers and amplify the demand for more grassroots development and professional opportunities. Key Highlights from India’s World Cup Campaign Conclusion India’s victory in the ICC Women’s World Cup 2025 stands as a watershed moment in the nation’s sporting history. The remarkable all-round display by Shafali Verma and Deepti Sharma, guided by coach Amol Mazumdar, consummated years of progress and determination. With new stars, robust support, and rising investment, the future of women’s cricket in India looks brighter than ever

BlackRock $500 Million Fraud: Telecom Scandal Explained

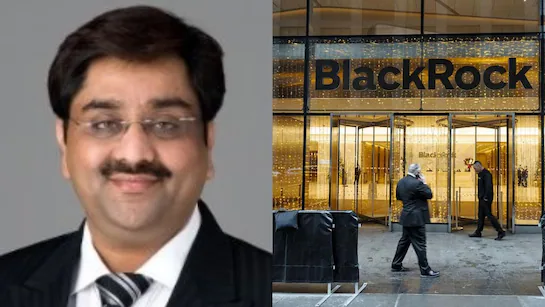

BlackRock Telecom Fraud: $500 Million Scandal Shakes Private Credit Market In October 2025, BlackRock’s private credit division was hit by a devastating fraud, resulting in a loss of more than $500 million. The deception was orchestrated by Indian businessman Bankim Brahmbhatt through his telecom-financing firm, Carriox Capital. Using fabricated documents and sophisticated digital tactics, Brahmbhatt created the appearance of financing legitimate receivables for prominent telecom companies, duping global lenders for years. How the Massive Deception Scheme Unfolded Carriox Capital claimed to fund telecom receivables for industry giants like T-Mobile, Telstra, and Telecom Italia Sparkle. However, investigations later revealed that many of these contracts and invoices were entirely forged. Brahmbhatt went to extreme lengths to make the scheme appear authentic, including building fake email domains that closely resembled real telecom organizations. These domains enabled his staff to send fraudulent confirmations and correspondence to unsuspecting lenders. By using these falsified receivables as collateral, Brahmbhatt was able to secure hundreds of millions in loans from leading financial institutions, notably BlackRock and French bank BNP Paribas. The scheme relied on circular transactions and fictitious payments, masking the fraud from auditors for years. The Collapse: Discovery and Investigation The fraudulent operation began to unravel when due diligence checks detected discrepancies in Carriox’s paperwork and communications. Suspicious email addresses and inconsistencies in supposed customer correspondence drew attention, prompting lenders to launch a thorough investigation. Once the fraud was confirmed, BlackRock and other impacted lenders swiftly pursued legal action, demanding repayment of the $500 million lost to the scam. Further scrutiny revealed the depth of the conspiracy: every customer email provided by Brahmbhatt’s companies over the past two years was forged, with some falsified contracts stretching back to 2018. Lenders also claim Brahmbhatt secretly moved pledged assets to offshore accounts in India and Mauritius, making recovery even more difficult. Executive’s Disappearance and Bankruptcy Filings As the investigation reached its peak, Brahmbhatt vanished from public view. When BlackRock’s team visited his New York office, they found it deserted. Shortly after a major news report exposed the scheme, Brahmbhatt deleted his social media accounts and became untraceable. Industry insiders believe he fled to India, leaving his businesses and lenders in turmoil. On August 12, 2025, Brahmbhatt declared personal bankruptcy, coinciding with his companies seeking Chapter 11 protection. Associated entities, Carriox Capital II and BB Capital SPV, also entered bankruptcy proceedings, complicating the legal battle for lenders. Impact on Global Lending and Private Credit Market The scandal has triggered alarm throughout the private credit industry, especially in asset-backed lending where revenue streams serve as collateral. BlackRock’s loss, while significant, represents only a fraction of its $179 billion private credit portfolio, but it underscores the risks tied to rapid expansion and reliance on borrower-supplied documents. BNP Paribas, which financed nearly half the disputed loans, increased its loan loss provisions by €190 million in its recent financial disclosures. The bank declined to specify whether this relates directly to Carriox, but industry observers believe the connection is clear. Telecom fraud schemes like this expose how digital manipulation and well-planned counterfeiting can bypass controls, especially when verification depends heavily on borrower-provided information. Cases such as Carriox highlight the urgent need for more robust due diligence, better digital verification tools, and greater industry collaboration to detect and prevent large-scale financial deception. Lessons for the Industry: Preventing Telecom Fraud The telecom and lending industries must take away crucial lessons from this event. BlackRock Telecom fraud comes in many forms, from fabricated invoices and identity theft to more intricate schemes exploiting digital channels and email spoofing. Prevention strategies now include: As fraudsters adapt new technologies to their schemes, companies must stay ahead of emerging trends by constantly updating their fraud detection and response strategies. What’s Next for BlackRock and Lenders? Legal proceedings against Brahmbhatt and his companies are ongoing. Recovery of the stolen funds will be challenging, given the complexity of the offshore asset transfers and bankruptcy filings. Lenders are expected to tighten controls, implement advanced verification processes, and commit resources to minimizing their exposure to similar risks in the future. Meanwhile, this case stands as a stark warning: rapid growth in private credit and telecom finance brings new opportunities—and new dangers. The BlackRock fraud scandal will likely spur long-term changes across financial institutions and the telecom sector, with enhanced vigilance and technological upgrades at the forefront of risk management. For more insights, subscribe The Business Tycoon

Beyond Chatbots: How Generative AI is Reshaping Human Creativity

The past few years have witnessed an unprecedented rise in artificial intelligence, but one branch has captured the imagination of creators, businesses, and technologists alike, generative AI. While AI once meant predictive analytics, automation, and chatbots answering FAQs, it has now leapt into the realm of art, music, design, literature, and even film production. Generative AI is no longer just a support tool; it’s becoming a co-pilot in the creative process. But what does this mean for human creativity? Is AI replacing us, or is it expanding the very definition of creativity in the 21st century? The Evolution of Generative AI: From Code to Canvas Generative AI refers to systems trained on large datasets that can create new content, text, images, video, code, or even music, that feels original and human-like. Early AI systems focused on repetitive automation, but generative models such as GPT (text), DALL·E (images), Stable Diffusion (art), and Jukebox (music) have broken the boundaries between human imagination and machine learning. In essence, we’ve moved from AI as a tool of efficiency to AI as a partner in creativity. Generative AI in Creative Industries Visual Arts & Design Tools like DALL·E 3, MidJourney, and Stable Diffusion are helping artists generate concepts in seconds. A designer can input “a futuristic cityscape at sunset with neon reflections,” and AI produces multiple unique versions instantly. This is not about replacing artists but enhancing their workflow, AI helps overcome creative blocks, explore visual styles, and generate fresh inspiration. Writing & Storytelling Generative AI has entered publishing. Authors use AI to draft plots, create character backstories, or even polish prose. Screenwriters experiment with AI-driven dialogue suggestions, and journalists lean on AI for research and fact-checking. Far from erasing originality, AI is accelerating the brainstorming process, allowing writers to focus on refinement and emotional depth. Music & Sound Production Platforms like AIVA and Jukebox generate symphonies, soundtracks, or commercial jingles. A filmmaker no longer needs a full orchestra to test background scores, AI can compose samples instantly. Musicians use AI to break out of repetitive patterns and explore new genres. Film & Animation AI can storyboard, create synthetic actors, and even generate CGI effects. Disney, Netflix, and other studios are already experimenting with AI-driven workflows. While the director’s vision remains paramount, AI cuts costs and time in pre-production and post-production stages. Fashion & Architecture From virtual fashion runways in the metaverse to AI-powered architecture designs optimizing space and sustainability, generative AI is shaping industries that blend aesthetics with function. The Psychology of AI-Enhanced Creativity Some fear AI will dilute originality, but psychologists argue it’s redefining the creative process. Creativity has always involved building upon existing ideas, from Renaissance painters inspired by their peers to musicians remixing cultural sounds. Generative AI mirrors this process at scale. In short, AI does not remove human creativity; it augments it by expanding the possibilities available. The Benefits of Generative AI for Creators The Ethical Dilemmas of AI Creativity While the benefits are undeniable, the rise of generative AI brings serious ethical challenges: Balancing innovation with ethical responsibility will define the trajectory of AI in creative spaces. Human Creativity vs. Machine Creativity One key question arises: Can machines truly be creative? Creativity in humans involves emotions, lived experiences, and intuition, things AI doesn’t possess. AI generates patterns, not personal meaning. A painting may look beautiful, but it lacks the human intent of telling a story born from struggle, joy, or love. Thus, rather than replacing creativity, AI highlights the uniquely human aspects of art and innovation. The most powerful creations will come from human-AI collaboration, where machines provide scale and speed, while humans provide depth and meaning. Case Studies: Generative AI in Action These examples show that AI is not a replacement; it’s a new creative medium. The Future of Generative AI in Creativity Looking ahead, several trends are emerging: Generative AI won’t end human creativity; it will reshape it, expand it, and push it into uncharted territories. Conclusion: Creativity in the Age of AI Generative AI has already moved beyond chatbots and predictive analytics. It now paints, writes, sings, and designs alongside us. Instead of diminishing human ingenuity, it offers a canvas of infinite possibilities, where technology amplifies imagination. The future will belong not to humans or AI alone, but to those who can merge the two into something extraordinary. Just as photography didn’t kill painting, and digital art didn’t erase traditional art, generative AI won’t erase human creativity. It will redefine it for a new era, an era where imagination has no limits. For more insights, subscribe The Business Tycoon

Digital Car Key Technology: Samsung Partners with Mahindra for Next-Gen Electric SUVs

Samsung’s rollout of Digital Car Key support for Mahindra Electric Origin SUVs is set to redefine how Indian consumers approach vehicle security and convenience. Powered by Samsung Wallet, this integration allows users to lock, unlock, and start select Mahindra electric SUVs directly from eligible Samsung Galaxy smartphones, removing the need for physical keys. Key Features: Advanced Technology and Security Market Impact: Growing Digital Key Adoption The market for digital automotive keys is surging, forecast to grow from $1.7 billion in 2023 to $9.5 billion by 2033 at an annual rate of 18.8%. Luxury automakers have widely adopted proprietary digital keys, but Mahindra’s integration with Samsung Wallet marks a major leap for accessibility and user convenience in India—a move expected to disrupt market norms and accelerate smart car adoption. How It Works: Seamless User Experience Security First: Protection From Start to Finish Samsung’s Knox platform delivers robust security that goes beyond conventional passwords. All digital keys are encrypted and stored within Samsung Wallet, protected by hardware-based defenses and two-factor authentication options. If a device is misplaced, users can instantly revoke key access or wipe encrypted data to ensure the vehicle remains secure. Growing Galaxy Ecosystem Samsung has previously enabled digital car keys for brands such as BMW, BYD, and Mercedes-Benz, but its partnership with Mahindra signifies a tailored approach for the Indian market. This cooperation reflects Samsung’s ongoing commitment to expanding connectivity within the Galaxy ecosystem, creating an all-in-one hub for payments, identification, and now secure mobility. Expert Perspectives Nalinikanth Gollagunta, CEO of Mahindra’s Automotive Division, emphasized the company’s vision for first-class innovation and customer experience in India’s EV sector. “Our Electric Origin SUVs have captivated our customers with advanced features and futuristic design. Partnering with Samsung brings another first-in-class convenience digital car keys—that makes every journey smarter and safer,” he said. Madhur Chaturvedi, Senior Director for Services & Apps Business at Samsung India, added, “This partnership delivers on our promise of seamless, connected, and secure experiences for Galaxy users, making daily activities like driving more hassle-free”. User Experience: What Owners Can Expect Conclusion: A New Era for Indian Mobility The Samsung-Mahindra partnership ushers in a new epoch for automotive convenience and security in India. Digital car keys not only enhance daily user experience but also showcase the potential for smarter, greener, and more connected transportation. This innovation is set to drive both brands’ reputations as pioneers in the digital transformation of mobility—changing how millions engage with their vehicles. For more insights, subscribe The Business Tycoon

Reviving Downtowns: How Urban Renewal Is Attracting Young Buyers

Cities are changing beneath our feet. Once-dormant downtowns, places that felt like ghost towns after 6 p.m., are waking up with coffee shops, coworking floors, pocket parks, and late-night food vendors. What’s driving that energy? A mix of smart policy, creative reuse, and an evolving generation of young buyers who want walkability, community, and meaning from where they live. This article explores how urban renewal is reshaping downtowns and why younger homebuyers are leading the charge. Why young buyers care about downtowns Young buyers, Millennials, and Gen Z, arrive with different priorities than previous generations. They grew up with smartphones, rideshare apps, and heightened awareness of social and environmental issues. Several consistent preferences shape their housing decisions: Urban renewal that responds to these preferences creates a powerful magnet for young buyers. Strategies that make downtowns desirable again Urban renewal isn’t one-size-fits-all. The most successful downtown comebacks blend physical improvements with policy incentives and cultural investments. Here are the proven strategies for drawing in younger buyers. 1. Adaptive reuse and mixed-use development Turning old warehouses, factories, and office blocks into mixed-use developments creates authentic, character-rich spaces that appeal to buyers tired of cookie-cutter suburban neighborhoods. Adaptive reuse preserves architectural heritage while introducing apartments, retail, and communal spaces, ideal for young buyers seeking unique homes with stories and character. Mixed-use developments place housing over shops, cafés, and studios, fostering 24/7 activity. That vibrancy is exactly what young buyers want: convenience plus the feeling that the neighborhood is alive. 2. Placemaking and public space activation Activating streets and public spaces, through plazas, street art, outdoor seating, and pop-up markets, changes perceptions overnight. Placemaking treats the downtown as a stage, inviting events, farmers’ markets, nighttime performances, and weekend festivals. These place-based initiatives create shared experiences that attract young people who value social life and discoverability. Small interventions, like parklets, weekend vendor zones, or pedestrianized blocks, can have outsized impacts on perceived safety and desirability. 3. Transit-first and micro-mobility integration Easy access to transit is a huge selling point. Urban renewal projects that prioritize transit connections, bike lanes, and micro-mobility (e-scooters, bike-share) reduce reliance on cars and appeal to environmentally conscious buyers. Transit-oriented developments concentrate housing and amenities near rail, tram, or major bus routes, cutting commute times and increasing accessibility to job centers and cultural hubs. 4. Affordability through diverse housing options Attracting young buyers requires a palette of housing types, micro-studios, co-living spaces, affordable apartments, and starter condos alongside market-rate units. Public–private partnerships, inclusionary zoning, and creative financing (like shared-equity models) help maintain affordability while enabling development. When downtown revitalization includes affordable pathways, it draws a broader and more vibrant population. 5. Incentives and policy alignment Municipal incentives, tax abatements, brownfield remediation funds, and flexible zoning can unlock redevelopment of underused properties. Simplifying permitting and fast-tracking projects that include public benefits (affordable units, public plazas, childcare centers) encourages developers to build in ways that align with community goals. Transparent, consistent policy reduces developer risk and gets projects built faster. 6. Safety, lighting, and 24/7 activation Perception of safety is a baseline requirement. Renewal that introduces improved street lighting, active ground-floor uses, and programming that keeps streets used at different hours reduces the “dead downtown” feel. Safety improvements are often social as well as physical; community policing models, neighborhood ambassadors, and coordinated maintenance all make a difference. 7. Creative financing and community investment Crowdfunding local projects, community land trusts, and impact investors can help finance reimagined downtown spaces that traditional lenders might avoid. When residents can invest in their own neighborhood (financially or through sweat equity), they build stronger, lasting ties, an attractive prospect for young buyers seeking meaningful community engagement. Design features that speak to younger buyers The built environment matters. Young buyers gravitate toward dwellings and neighborhoods designed with contemporary lifestyles in mind: When developers and planners combine these features with authentic local culture, they produce places young buyers want to call home. The social and economic ripple effects Revived downtowns don’t just sell homes; they catalyze broader economic and social benefits: Pitfalls to avoid Not all renewal is beneficial. Without care, redevelopment can produce displacement, homogenization, and loss of local identity. Common pitfalls include: Combining community engagement, anti-displacement strategies, and localized design prevents these outcomes. How cities can make renewal work: action checklist For municipal leaders, developers, and community groups aiming to attract young buyers while building an equitable downtown, here’s a practical checklist: A vision for the future Imagine a downtown where a morning run takes you through a renovated rail yard turned linear park, where you stop at an independent café run by a local entrepreneur, swipe into a sunlit apartment that doubles as a remote-work studio, and close the day with a community music night. That vision isn’t pie-in-the-sky; it’s the direction many successful renewals are taking. To attract young buyers, downtowns must offer more than a roof over one’s head: they must deliver connection, convenience, authenticity, and the ability to shape place. When policymakers, developers, and communities collaborate, centering equitable access and local identity, revived downtowns become engines of opportunity rather than engines of displacement. Closing thoughts Urban renewal that centers on people, walkable streets, mixed uses, affordable housing, and activated public life aligns beautifully with what young buyers want: a life that’s convenient, meaningful, and engaged. Cities that carefully manage growth to lift existing residents while welcoming new ones will create downtowns that are not only desirable but also just and resilient. For developers, planners, and civic leaders, the work is clear: build places that people want to live in, places with texture, access, and heart, and the young buyers will follow. For more insights, subscribe The Business Tycoon